Since the ATF announced last Friday (January 13, 2023) that the publication of the final arm brace rule (2021R-08F) was imminent, there has been a flood of online rumors regarding how the rule will be implemented and enforced.

Since the ATF announced last Friday (January 13, 2023) that the publication of the final arm brace rule (2021R-08F) was imminent, there has been a flood of online rumors regarding how the rule will be implemented and enforced.

In that time, I have been inundated with calls from clients seeking to make informed decisions about whether to register their arm brace equipped pistols and how to use their NFA trusts to do so.

During these calls, there are a number of questions that I am repeatedly asked … and there are some persistent rumors spreading with answers that do not coincide with the ATF’s published position.

I have listed a few of them below as well as the answer from the ATF FAQ. While they are known to be a mercurial agency, I believe their own publication is the best source for determining how they are looking at the new rule.

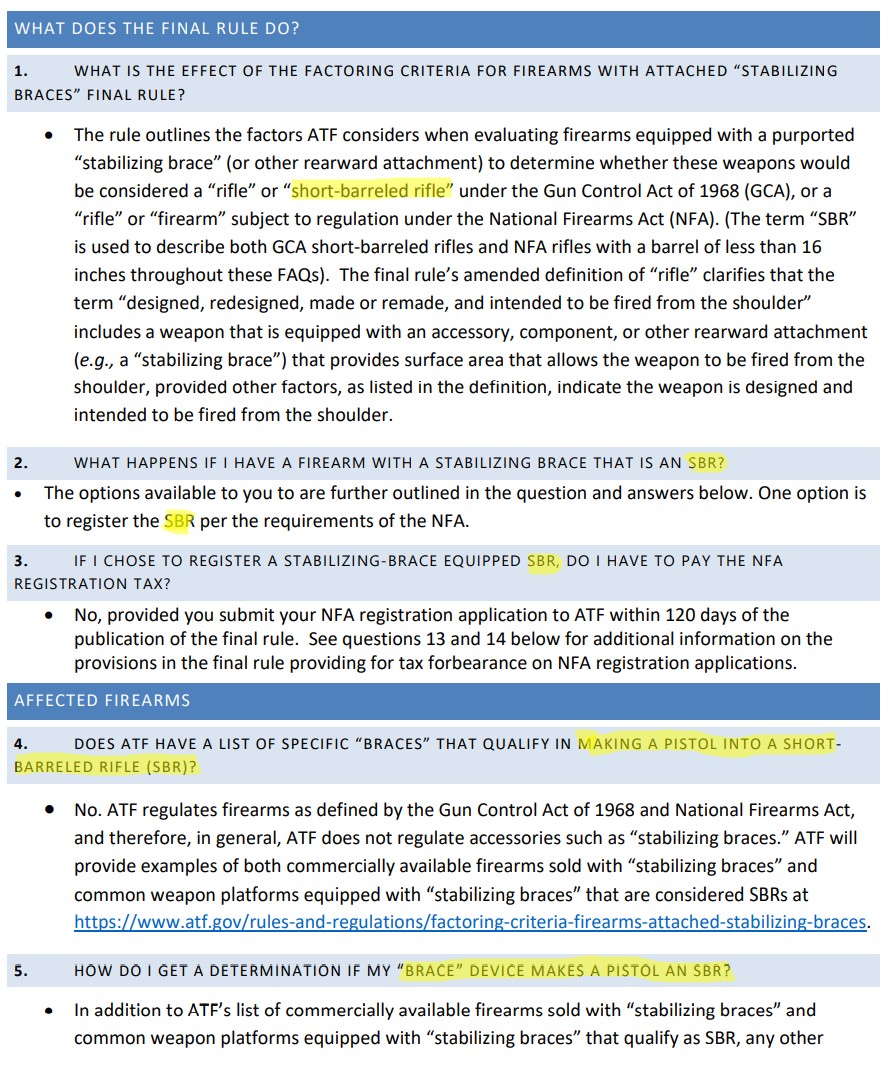

Question 1: Are they really letting us register brace-equipped firearms as SBRs or are they creating a new category called ‘braced pistols’?

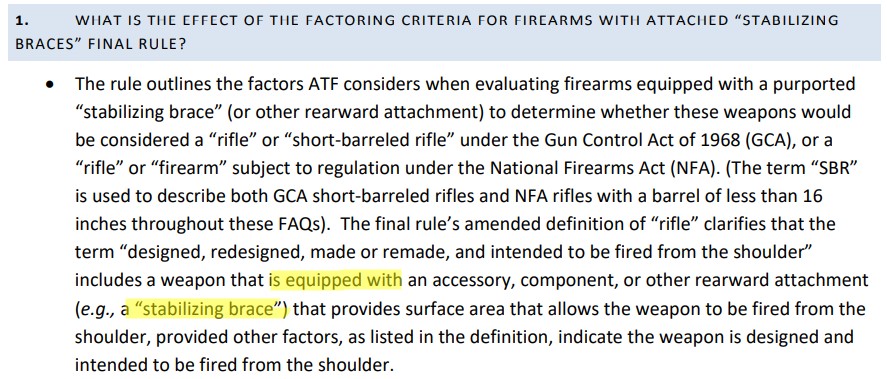

The rule states that many firearm models equipped with arm braces meet the definition of an SBR with the arm brace attached and therefore need to be registered as such. While an agency such as the ATF can promulgate rules that ‘clarify’ definitions from enabling statutes (in this case the NFA), they cannot add provisions to the law without congressional action.

In just the first page of the ATF FAQ (see screenshot below) they make it clear that what we are talking about is adding brace-equipped firearms to the definition of SBR.

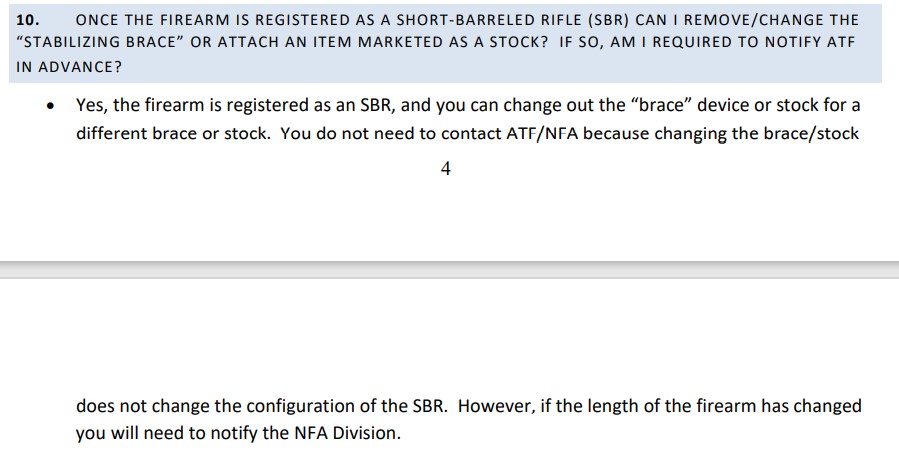

Question 2: If I take advantage of the free tax stamp, will I be able to remove the brace and add a normal stock once it is approved?

Yes. Despite the internet rumors to the contrary, the ATF FAQ (see screenshot below) clearly states that once it is registered as an SBR, you may feel free to remove the brace and add a stock.

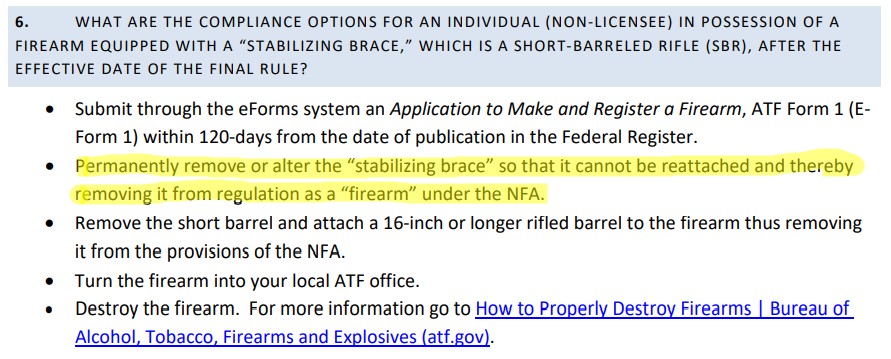

Question 3: If I remove and destroy the brace, will the firearm itself still be considered an SBR?

If you remove and destroy the brace then the firearm no longer meets the expanded definition of an SBR.

In addition, they specifically address this question in their compliance section.

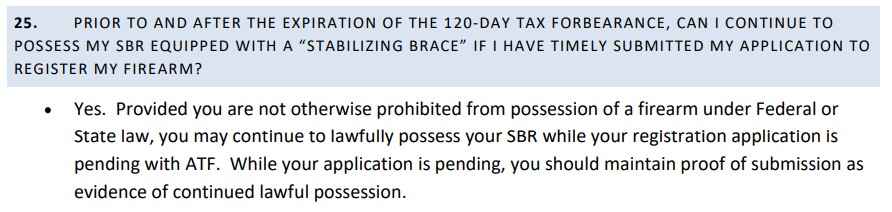

Question 4: If I have submitted my Form 1 for my free tax stamp but haven’t received it within the 120-day amnesty period, may I still keep the brace on my firearm while waiting for my tax stamp?

Yes … provided that you have submitted your application (and have proof of your submission) during the 120-day period.

I will do future posts as I continue to work with my clients to address their concerns about this rule.